Lending and borrowing; they seem like a practice as old as the human race. As long as people have had things, other people have needed those things and borrowed them for a returning favour. Whether this is your neighbour’s drill or a £500 loan from your friend, you’re expected to give the £500 back at some point and you’ll probably let your neighbour borrow that tool he needs too. All of this makes for a homely neighbourhood, with goodwill and good intentions saturating the air.

Now imagine that your neighbour had let you borrow his drill, but in return he not only wanted to use your lawn mower, but he wants you to gift him your set of screwdrivers too, just for the trouble of lending you his drill. I’m sure it wouldn’t be long before this kind of behaviour built up into a neighbourly dispute and before you know it, hedges are being lopped and gnome heads are rolling in the dead of night.

It seems like quite an obvious social contract; don’t exploit those you live with or rely on. Even just a natural law of “don’t be exploitative (or an expletive)” could be applied. So why in our modern society are these kinds of deals, reliant on interest rates and loans, so commonplace? It’s how every economy works, it’s the main process of banks. The practice of lending with interest enabled European countries to win wars and rise to prominence.

Even the International Monetary Fund (IMF) runs on the exploitative principles of interest and debt, a concept encapsulated in the neoliberalist, economy-first ideas of many modern governments. Throw in the ease at which you can now hoard and hide money, thanks to digital banking and shell companies and you have yourself a problem. It affects our culture and our rational reasoning to the point where we are already having international disputes over drills, hedges and borders, although now we are talking about military drills, hedge funds and national borders. Whether heads begin rolling remains to be seen.

All the way back in ancient Greece, the famous philosopher Aristotle was bad-mouthing a thing called usury; he called it “most unnatural” and “the most hated sort of [money-lending]”. And he wasn’t the only one. The great Italian writer Dante Alighieri described usurers in his Divine Comedy as “the last class of sinners that are punished in the burning sands” and placed them in the lowly seventh circle of his Hell. This money making practice was even banned by the Catholic Church “in the eyes of God” as well as “in canon”, on the grounds that it was exploitative. The Roman Emperor Cato the Elder even said that to demand interest of someone “is the same as killing a person”.

But What Is Usury?

Over the centuries people have defined usury in many ways, but it can literally be defined as making money from money; for example a loan on which the return is greater than the principal investment – usually done through the charging of interest. In contrast, a non-usurious loan was where the amount loaned out and paid back were the same. Confusingly interest on a late repayment could be agreed upon, to dissuade a late return, but the loaner of the money was not expected to want this outcome (and certainly not manufacture circumstances that would result in late repayment and therefore any accumulated interest). If you charged interest with the sole aim of actually collecting on this interest then the loan was deemed usurious.

This loose definition is why usurious loans were often a scourge of the poor, as they found themselves in situations where they could not pay back the initial sum by the due date despite their best intentions, and therefore they were at the mercy of any interest rates. As for the loaners, they were often already flush with cash, money-lending being a business one can only indulge in if one has funds to begin with. Therefore it became increasingly common for merchants and their progeny as inheritors of the family fortunes, to invest and loan. With the rise of venture capitalism in the late middle ages (and the resultant rise in for-profit companies and imperialism), usurious contracts soon became the accepted norm and before long central banks had been created and whole nations suddenly found themselves with mounting debts and interest rates.

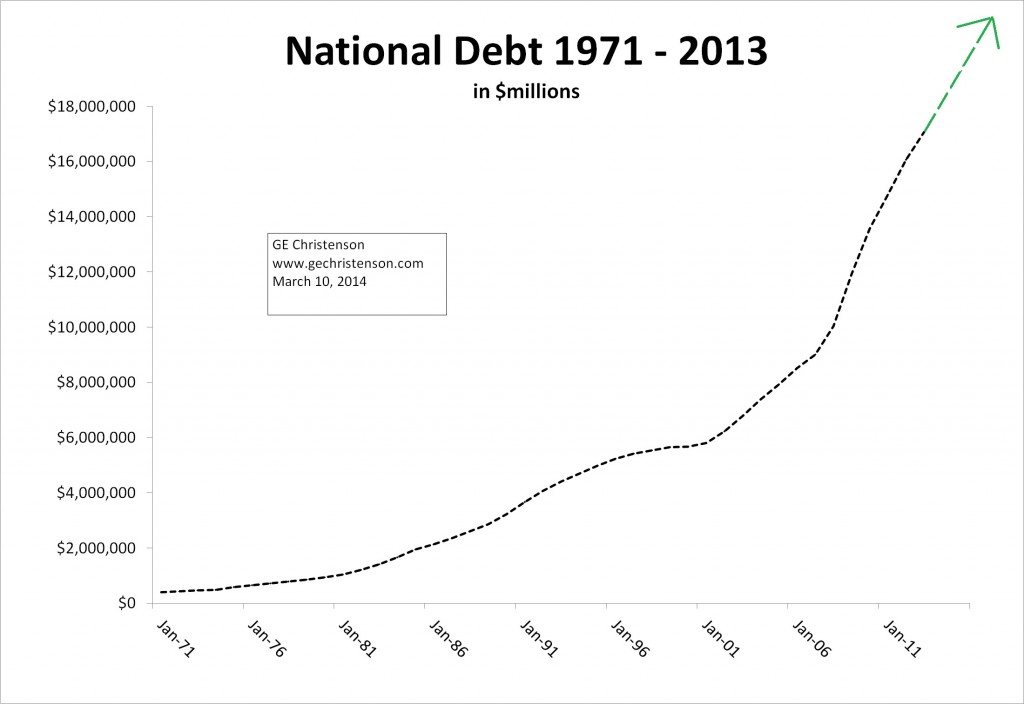

National debt was non-existent before the creation of the Bank of England.

When it was created in 1694, to help fund wars against Louis XIV, the national debt was £1million.

By the time of Louis XIV’s death in 1715 it had risen to £50million.

By the time of the Seven Years War in 1756, it was nearly three times this at £140million.

The American Revolution twenty years later added yet another £100 million to an already gargantuan growth spurt, taking Britain’s National Debt to 222% of its gross domestic production.

The lending and collection of usurious loans require no labour or effort on the part of the lender, with profit almost always coming at the expense of others.

Because of its exploitative nature, money gained through usury was seen as an immorally acquired fortune by religion, society and nature until around the 1700’s when definitions of usury began to be manipulated and twisted. The laws around usury have historically allowed for quite large grey areas, which have long been exploited in order to transfer wealth from one person or group to another.

Definitions and whether loans were acceptable was largely at the judgment of a community or court, and so, as merchants became more powerful and trading companies held more economic sway, the definition of usury was changed to allow more profiteering by those with money to lend. The creation and implementation of institutions like the Bank of England that control this lending and borrowing helped streamline the process, while making the whole exercise seem like a natural necessity. However in order for this to happen, public opinion needed to be changed. How else do you go from usury being akin to killing someone, to its acceptance as an integral part of society?

The Enlightenment of Entitlement

Ironically, the enlightening ideas that led to individualism and the humanist revolutions of the late middle ages may have been the start of the slippery slope towards acceptance of usury’s exploitative nature. A rise in the importance of the individual, thanks to Martin Luther’s translation of the bible and thinkers (therefore they were) such as René Descartes, meant that the power of the church was declining and so were it’s associated power structures. In its place rose individuals, with money and power, who proceeded to build institutions that benefited “man” rather than “men”. The writers Rousseau and Hobbes highlight these cultural changes, from “men” to “man” in their writings, promoting the idea of the self as well as a commonwealth of individuals to protect these individual interests respectively.

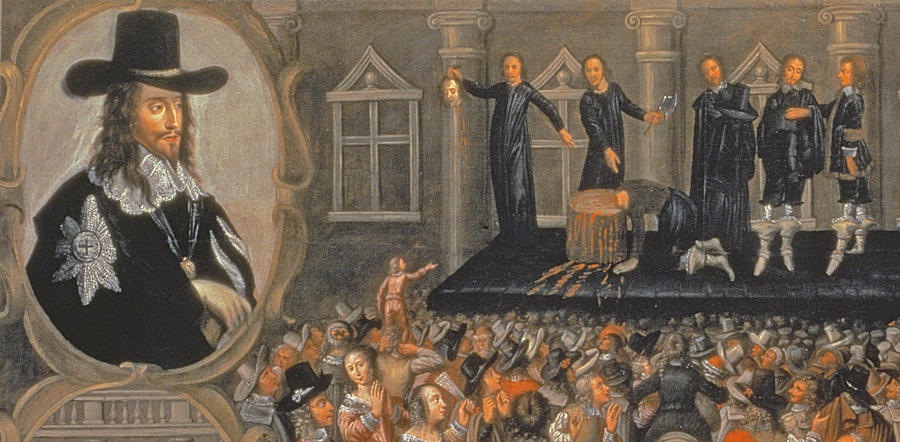

In the case of Thomas Hobbes, his book Leviathan developed this theme and became the main argument for the creation of Britain’s parliament. A parliament that went on to behead its king (for the first time in British history), importing in his place a Dutch king more sympathetic to the economic hunger of the English merchants. The resultant economic practices and institutions are still commanding the economy today.

As Western thinkers looked through history to find a way to enliven usury’s public image, they came across an idea that is unfortunately as antiquated as usury itself; Antisemitism. Through the anals of history, the Jewish people have had a well documented time being excluded, exploited and exterminated. Like many refugees, they often immigrated with degrees and professions, but like so many refugees, ended up having to take menial jobs in their adopted homelands. Many became competent traders, so much so that others were often intimidated by the competition and Jewish merchants found themselves pushed out of reputable professions through propaganda and the passing of discriminatory laws. Heavy penalties for breaking these laws and the risk of sparking another murderous pogrom meant that Jewish people were often pushed into shadier methods of making money. One such method was money-lending. The Jewish people have always been easy prey for historians looking for a scapegoat and it was no different with British writers looking to spin public opinion on usury towards the end of the 1700’s.

The Path To Acceptance

First it was put forward that Jews were going against their own teachings of the Talmud by dealing usurious loans. Then, that the “general and violent” nature of these money-lenders left the “ignorant” and less intelligent “clergies of ancient churches” to deem usury a sin. Encapsulated in their own “age of darkness and superstition”, the impression put forward by writers like J.B.C. Murray, was that the masses and their advancements in trade stagnated. According to scholars of the time, it is only in the light of modern European “excellence” and commerce that we can now see usury’s true value.

Not content with using just one of Europe’s favorite crutches to back their argument, writers would often hark back to Ancient Greece, the primordial soup of democracy from which Europe rose to prominence. Aristotle, remember, seemed quite certain in his negative views on usury however, in Murray’s argument, he manages to paraphrase Aristotle in such a way that Aristotle’s vitriol for usury is masked. It instead comes across as a mild comment on usury, making no mention of the unnaturalness attributed to the practice by the great Greek thinker. Where negative Greek and Roman sentiments on usury are quoted, they are often left in Latin or Greek. If they are translated, the language is much watered down or surrounded by vague language. By relating the acceptance of usury to Ancient Greece and Rome, writers such as Murray and Gerhard pander to the Anglo-Saxon need for validation from the ancient, perceivedly white world.

After the ancient world’s acceptance of usury was manipulated into being, acceptance by the church was next. The 14th century scholar Jean Charlier de Gerson was the next target for writers on usury. Described as “the most eminent and devine of his day” by Murray, he apparently spoke “very fully upon the theme of usury”. According to modern scholar Johan Gerhard, writing in 2019, Gerson spoke with “eloquence, moderation & fairness” on the matter and pushed for its acceptance in trade and society. Throughout both papers, Gerson is a staunch advocate for the installation of interest rates, citing “the vulgar”as well as “the scholars” as reasons for usury’s misunderstood nature.

In reality Gerson never spoke so fully on the subject of usury that it is ever mentioned in any biographies. In fact all references to Gerson and usury that I found in my research was exclusively limited to pro-usury papers like Murray’s and Gerhard’s. Gerson was better known as being the first western thinker to develop the contemporary idea of natural rights. This did include thoughts on interest and loans, but he advocated the recognition of “intention” in money lending. Gerson’s idea harks back to ideas of “unnatural” and “natural” exchanges, as he was more interested in the morality of a loan and how any interest would affect the borrower. If the intent of the loan is fraudulent – or in other words – if the loaner intends to collect on the interest rather than just the amount lent the the loan should be deemed usurious; as it would be unnatural in the eyes of natural morality and god.

Far from being a friend to commerce, it is said by more reputable scholars of Gerson that he had “moved well beyond the earlier medieval dislike for merchants”, as in his view, it was “impossible to avoid sin” while in the business of trade. Instead he believed that trade was established for the “common advantage of both parties”. This sentiment was backed by laws of the time restricting usurious contracts and Gerson was in favor of this status quo, speaking for leniency rather than reform on the matter.

Unfortunately for history, Gersons ideas were often extrapolated into revolutionary sentiments. His thoughts on natural law were used to justify the rights of religion, the state, and the individual. From The Rights of Man which preceded the American Revolution (which was itself sparked by the British crown pushing usurious contracts onto its American colonies) to Wealth of Nations, Gersons ideas were increasingly turned towards any scholarly argument of the time. His name was synonymous with the “natural order” of things, and so any concepts attributed or linked to him became socially and morally accepted by western society through osmosis.

One key idea that resurfaced at the time of colonialism was that of two 15th century theologians; Bernadine & Antoninus. They posited that interest, so far only due on late repayments, should begin to accrue from the very beginning of the loan. In other words, the repayment would always be greater than the loan. The amount of interest one could add was subject to the amount of risk on the loan, with higher risk allowing a higher interest rate. Fortunately this was an opinion held by the minority at the time, however you may recognise it as the way interest is implemented in our modern society. The thinking behind this was that a lender should be reimbursed for the profits which they could have made, had they kept the loaned money in their business. This essentially enabled and encouraged even the most financially unstable merchants to lend sums of money as they were always guaranteed a profit on it’s return. The lender effectively shared none of the risk and actually could profit from a riskier loan as the chances of losing their money was greater. This approach encouraged lenders to boost the perceived risk of a loan, as the higher the risk, the higher the interest they could charge.

While not embraced in their time, the ideas of Bernadine & Antoninus were fully embraced by the new economic state of the British ushered in after the beheading of Charles I and the Glorious Revolution of 1688. The ability for any merchant to lend and gather a fortune at the expense of others, with high levels of interests hidden as “risk fees” started the ball of unfettered capitalism rolling towards imperialism, and it wasn’t long before Britain was using it’s financial might to control the globe. The argument for Britain’s rise to power in the 1700’s is usually attributed to naval power and democracy, but maybe it has more to do with them turning their backs on the moral values laid down by history.

With the subsequent rise in trades like slavery and the creation of banks to guard these fortunes, it is not hard to see how a small change to societal views on usury snowballed into a modern society that has no qualms sending bailiffs after pensioners and taking away the homes of those in need. After all, repossessions are examples of a bank’s rights coming before those of the individual.

What would Gerson have to say about such things?

Spinning The Web

Throughout Britain’s rise to power, the ceiling on the levels of acceptable interest was increasingly skirted by inventing risk, fictitiously increasing the sum of the initial loan, issuing bonds below par, playing with exchange rates and adding profit sharing elements. This appreciation for grey areas is something that has catapulted and secured Britain (or at least the City of London) into a position of economic dominance that it still holds on to.

Throughout Britain’s rise to power, the ceiling on the levels of acceptable interest was increasingly skirted by inventing risk, fictitiously increasing the sum of the initial loan, issuing bonds below par, playing with exchange rates and adding profit sharing elements. This appreciation for grey areas is something that has catapulted and secured Britain (or at least the City of London) into a position of economic dominance that it still holds on to.

While stigma against the accumulation of wealth and the addition of interest likely existed long before Aristotle wrote it down into western scripture, nowadays it’s the modus operandi of our financial systems. It’s how sovereign countries are able to trade with each other and the idea of interest, beginning at the start of a loan, is accepted as a fact of life. The IMF and World Bank, tasked with bringing nations into the free market and the modern trading world, does so through usurious loans that developing countries can often only dream of paying back. Economic Historian Dr Michael Hudson refers to the euphemism of “development”. In this context calling it instead a forced dependency on Western exports and finance (a cursory google of the chemical and agricultural company Monsanto’s actions in developing countries such as India show many instances of this systematic abuse).

The rules set by the IMF, that countries must follow, can often damage and devalue the nations assets and industries. This is achieved by first imposing strict regulations which must be followed in order to receive the loan. In order to adhere to these regulations the country often accrues more debt. This is on top of the interest on the loan from the IMF. Finally the country is then encouraged to open up to the private sector, whereby all the assets and money are transferred to a handful of owners through the acquisition of debt and industry.

While not strictly the IMF, similar tactics were clearly demonstrated by the US in their relations with Russia at the end of the Cold War. Gorbachev finally agreed to open up Russia to western markets in return for peace. The result of this decision was an exorbitant, almost biblical rise in national debt. Rising from $0 to tens of millions in a matter of years under Boris Yeltsin and the transfer of all of Russia’s wealth to a handful of oligarchs.

Unsurprisingly, for developing countries with little to no other choice, the rules and regulations imposed by the IMF only ever seem to exacerbate problems. The rules increase the amount of money leaving the country in flight-capital while bleeding the country’s resources dry. A case study into any western nations activities in any African, South American or Asian nation (e.g. French influence in Mali, the British in India, US operations in Latin America) turns up instances of foreign intervention, flight capital, and a sinking sovereign ship left to the overwhelming tides of the free market – all while still in massive debt to the IMF despite the removal and sale of its resources. If you could point me towards a developing country who’s people are healthier as a result of help from the IMF, not just it’s economy, I would be very interested to read that case study.

How we came to accept this state of affairs is a road littered with manipulation and malpractice. As seen with Gerson and Aristotle, even those seeking to create a fairer world with their words can posthumously have them twisted into supporting an argument that would have the original authors spinning in their graves. Flying in the face of morality, our current concept of capitalism towers tall over everything else.

This seems to include morality and natural law.

Businesses have more rights than the people they apparently serve and corporations create the laws through excessive and expensive lobbying of governments. Governments that can’t or won’t be lobbied are often overthrown and interest accrued from the first handshake is the norm in business, unfortunately becoming the norm for all.

This doesn’t even touch on how this usurious system of interest and borrowing has developed into the creation of public and national debt, which themselves have become tradable commodities.

All of this can be summed up as profit at the expense of others, which to those “vulgar” and “ignorant” masses of earlier times, was not an acceptable state of affairs. If ignorance is bliss by way of economic stability, I’ll take it over student debt and credit cards.

Re “ignorance is bliss”…

Ignorance of the reality of lies and deceptions (=most mainstream news and establishment decrees) is bliss because exposing yourself to that is self-propagandization.

Ignorance of truths (especially if they’re upsetting) is not, or only temporarily or rarely, bliss because it is ultimately self-defeating.

The FALSE mantra of “ignorance is bliss”, promoted in the latter sense, is a product of a fake sick culture that has indoctrinated its “dumbed down” (therefore TRULY ignorant, therefore easy to control) people with many such manipulative slogans. You can find the proof that ignorance is never bliss (only superficial fake bliss), and how you get to buy into this lie (and other self-defeating lies), in the article “The 2 Married Pink Elephants In The Historical Room” … https://www.rolf-hefti.com/covid-19-coronavirus.html

“Blissful” believers in “ignorance is bliss” — blissfully stupid people — are nearly always self-destructive indifferent immoral ignoramuses and/or members of herd stupidity… speaking of which, with the letters of “omicron” an alleged Covid variant you can spell “moronic”

And further speaking of stupid herd people not getting the glaringly obvious truth/ie not getting the constant onslaught of BIG lies of the official authorities……

“2 weeks to flatten the curve has turned into…3 shots to feed your family!” — Unknown

“If ‘ignorance is bliss’ –there should be more happy people.” — Unknown

LikeLike

Thanks for reading my article, however you seem to have latched onto the “ignorance is bliss” part quite hard. I’m not “promoting” the “mantra” of ignorance is bliss as you call it, I’m merely stating that stating people are “ignorant” is a way for later generations to brush aside the past, as it’s easy for us to think of those in the past as stupider than ourselves – ignoring the fact that going by our written record, we’d probably come across as pretty stupid to the layman of then too.

The point of ignorance is bliss in this context is to highlight that the age of “ignorance” as Murray called it was actually more enlightened with regards to economy and morality than we are today, so while I appreciate your adolescent ramblings about our broken society, I’m afraid here you have completely missed the end of the stick and fallen into the pond.

In my opinion it’s using language like “self-destructive indifferent immoral ignoramuses” to insult those with opposing views to your own, and writing opinions as unsourced quotes that is the truly damaging behaviour in our society. In this respect one is no different to Murray, who by all accounts was a self-centered tool of a man who may not have understood the lasting damage he helped create.

I hope you are not so ignorant that you do the same.

LikeLike